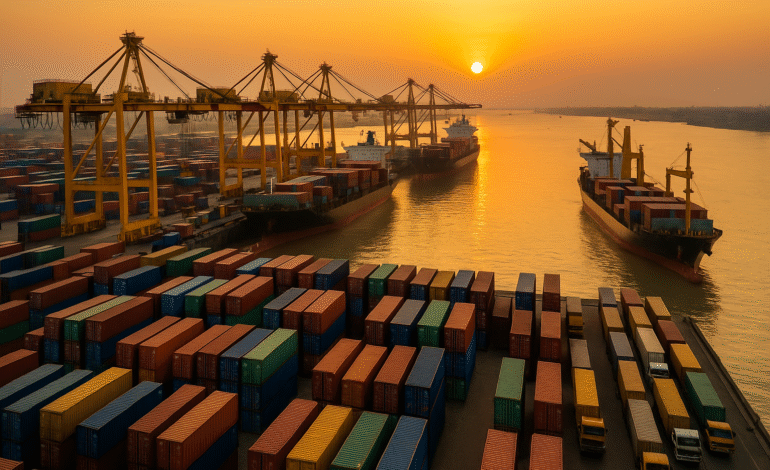

Will Tariff Hike Reshape Bangladesh’s Trade Landscape?

A sudden policy move that raises off-dock charges by 63 percent, together with an average 41 percent increase in Chattogram Port tariffs, is not a narrow tax on shipping, it is a structural shock to how Bangladeshi goods reach global buyers, and how imports feed local industry.

The central economic problem is clear that Bangladesh’s trade logistics cost is already high, and these hikes magnify that problem.

Exporters and importers face immediate per-container cost increases that translate into higher unit costs, narrower margins, higher retail prices, and potentially diverted trade flows. The country’s competitiveness gains in recent years, reflected in better World Bank Logistics Performance Index (LPI) standings, are at risk if the cost shock is not managed.

What the numbers say about the hikes and who pays?

The two headline measures announced in 2025 are concrete and measurable, they hit specific line-items of the supply chain. The Bangladesh Inland Container Depots Association (BICDA) revised package and handling charges that raise a typical 20-foot container package fee by about 60 to 63 percent, for example from Tk6,187 to Tk9,900 in one commonly reported schedule, with 40-foot containers seeing a similar jump.

Separately, the Chattogram Port Authority implemented an average 41 percent rise in port service tariffs, raising loading and unloading fees and other port service elements, effective mid-October 2025. These are not theoretical increases; they are real cash outflows per container for importers and exporters.

Immediate pass-through to exporters and importers, and why it matters

When off-dock and port charges rise by double-digit percentages, firms face two clear choices, absorb the cost, which reduces profit margins, or pass the cost on to buyers, which reduces price competitiveness. For Bangladesh export sectors that compete on thin margins, such as ready-made garments, footwear and light manufacturing, neither option is attractive.

Empirical microdata from port fee announcements show importers will pay roughly Tk5,720 extra per twenty-foot container under the new port schedule, and exporters an increase of about Tk3,045 per twenty-foot container, on top of existing freight, insurance and production costs. At scale, repeated over millions of TEUs annually, this raises cost-per-unit and creates incentives for buyers to look for lower-cost suppliers in the region.

Bangladesh’s trade logistics cost, the baseline problem

Before the hikes, Bangladesh already faced a heavy logistics burden, with logistics costs widely reported at 15 to 16 percent of GDP, well above the global average of 8–10 percent. High inland transport costs, congestion at Chattogram, long dwell times, and fragmented warehousing networks have combined to make moving goods unusually expensive in Bangladesh.

The tariff hikes add fuel to an existing fire, increasing the share of logistics in total landed cost for both imports and exports, and increasing working capital needs because higher port and handling fees typically increase inventory and dwell-time costs.

Channeled effects on prices, margins and trade competitiveness

At a micro level, consider a garment factory shipping a container that contains finished shirts to a buyer in Europe. Shipping and logistics form a nontrivial share of the total FOB cost. An extra Tk3,000 to Tk6,000 per twenty-foot container, depending on exporter or importer responsibilities, when converted to per-unit terms, raises unit costs and reduces exporters’ relative price advantage.

If Bangladesh’s logistics cost were already 15 percent of GDP, even a modest per-container rise will increase producers’ cost-to-serve, eroding the hard-won gains from improved compliance and productivity that fueled export growth in recent years.

Potential trade diversion to neighbors, and the regional comparison

Firms and freight forwarders make routing decisions on price, time, and reliability. If Chattogram becomes significantly costlier, shippers will evaluate alternative ports and corridors. Nearby countries offer contrasting combinations of cost and efficiency.

India has made steady improvements in its logistics performance, ranking much higher than Bangladesh in the World Bank’s LPI rankings, driven by major port investments, digitalization and hinterland connectivity. India’s better scores on timeliness and infrastructure make ports like Nhava Sheva and Mundra attractive alternatives for certain cargo.

Besides, Vietnam has become a particularly fierce competitor in labor-intensive manufacturing and exports, partly because of competitive port and hinterland costs and dynamic supply-chain diversification from China. Vietnam’s LPI ranking, around the mid-40s, reflects a more efficient trade corridor in several lanes, and logistics providers there routinely offer aggressive pricing for full supply-chain packages.

Cambodia, while not a major container hub, has had logistics costs estimated to be even higher as a share of GDP than Bangladesh, and its LPI rank is lower, underscoring that high logistics cost can be endemic where infrastructure and customs efficiency are weak. China, by contrast, maintains a large and highly efficient port system supported by scale economies, meaning its effective port charges per container can be lower relative to service quality for many routes.

Bangladesh’s logistics cost, the financing and working capital channel

Higher port and off-dock charges increase the cash tied up at port and in warehouses, a simple arithmetic effect. If importers pay an extra Tk5,720 per container, and typical lead times and dwell times are long, the working capital requirement for importers rises proportionally.

For exporters who receive payment on longer terms, higher pre-shipment handling and port charges mean more credit, or narrower margins if financing terms cannot be passed on. For sectors where lead time equals or exceeds buyer payment cycles, this constricts liquidity and could force small and medium enterprises to reduce production or exit, reducing export diversification.

Where some costs could be managed or mitigated

Not all the burden must be permanent. There are tactical mitigations logistics managers and policymakers can pursue. Better consolidation of shipments, renegotiation of freight contracts, smarter Incoterm use, and temporary tariff rebates for priority export lines can blunt the immediate hit.

Carriers and forwarders can also offer bundled door-to-door pricing that smooths the headline port shock. But these solutions only buy time; they do not substitute for reforms that lower the underlying share of Bangladesh’s logistics cost.

Best practices from regional peers show that infrastructure investment, digital port platforms, and faster customs clearance deliver sustained reductions in per-container cost.

Inflation and consumer price effects, a second-round risk

Higher import handling costs are not confined to industries that export. Import-dependent sectors, including raw materials, capital goods and fuel, will face higher landed costs, and some of that will pass through to final consumer prices, contributing to inflation.

In Bangladesh, where many households are sensitive to food and clothing prices, even modest cost increases in imports can have politically significant effects. The port tariff hike and off-dock increases therefore pose both an economic and a social policy challenge.

Bangladesh’s logistics cost, quantitative example to illustrate scale

To give a sense of magnitude: assume a firm imports 10 twenty-foot containers per month, an extra Tk5,720 per container raises monthly costs by Tk57,200, and annual additional outflows by roughly Tk686,400.

For an SME operating with a thin net margin, this sum can represent several months’ profit, or the equivalent of a working capital loan. Multiply this across thousands of firms and the aggregate effect is nontrivial, showing how per-container increases cascade into macroeconomic impacts.

This is why industry groups and chambers of commerce have been vocal in their objections, threatening slowdowns or coordinated actions unless tariffs are moderated.

Longer term competitiveness, lessons from regional neighbors

Neighboring countries show that reducing logistics friction depends on three pillars: coordinated investment in physical infrastructure, meaningful process reform and digitalization, and pricing that reflects efficiency gains rather than cost extraction.

India’s recent improvements have combined infrastructure upgrades with procedural reforms that reduced dwell times. Vietnam’s advantage rests on integration of ports with efficient trucking and inland container depots, and on strong private sector logistics capacity.

Bangladesh can learn from these cases, investing in port hinterland links, expanding private terminal capacity, and accelerating customs modernization to reduce the unit cost of trade even while tariff structures are recalibrated.

Risk of losing buyers, relocation and nearshoring

Buyers in Europe and North America routinely review supplier total landed costs. If Bangladesh becomes meaningfully more expensive than Vietnam or India on a comparable delivered basis, global retailers may shift orders.

Over time, persistent cost disadvantages can accelerate supplier relocation, undermining the gains from decades of foreign investment and factory upgrades in Bangladesh. This is an especially acute risk as buyers seek to diversify supply chains away from single-country concentration.

The Export Promotion Bureau (EPB) and trade policymakers may need to track such shifts closely to protect export growth momentum.

Bangladesh’s logistics cost, the policy trade-off and political economy

From a public finance perspective, port and off-dock tariff increases can be justified as a way to recover costs or finance upgrades. However, the timing and scale matter.

Sharp, unilateral hikes without phased implementation or targeted relief transfer the burden onto private firms at the worst possible moment, when global demand is volatile and margins thin.

A more sustainable approach would be a transparent cost-based tariff review, combined with a temporary moratorium for certain export-critical lines and an investment plan that delivers measurable efficiency gains.

Targeted reforms to reduce Bangladesh’s logistics cost over time

To lower Bangladesh’s logistics cost structurally, policy must tackle the root causes. Recommendations include faster digitization of port paperwork and customs clearance, expanded public-private partnerships for terminal operations, congestion relief through alternative gateways and inland dry ports, incentives for maritime carriers to offer competitive long-term services, and a transparent tariff formula that ties future increases to demonstrable improvements in dwell time or handling productivity.

The World Bank LPI improvements for Bangladesh in recent years show reforms can move the needle, but cost remains high, meaning further reforms should be accelerated and insulated from short-term fiscal objectives.

International financing and donor support as options

Multilateral lenders and development partners such as the Asian Development Bank (ADB) and World Bank often step in to finance port upgrades or provide technical assistance on customs modernization and digital platforms.

If tariff revenues are used to fund efficiency-enhancing investments, transparent project design and measurable KPIs can make the tariff increases politically and economically easier to accept.

The choice between revenue extraction and competitiveness

Bangladesh faces a choice: treat port and off-dock tariffs as a durable revenue lever or treat them as part of a broader competitiveness strategy that reduces Bangladesh’s logistics cost over time.

The immediate tariffs are a painful reminder that logistics is a central competitiveness variable. Policymakers can reduce long-term harm by linking tariff increases to clear productivity gains, by providing temporary relief to exporters and small importers, and by accelerating structural reforms that lower the per-container cost.

Otherwise, the short-term gain in revenues may be offset by longer-term losses in export volumes, employment and investment.

Call to Action

International buyers, multilateral partners and logistics investors should watch how Bangladesh manages the trade-off between short-term revenue and long-term competitiveness.

For exporters and importers in Bangladesh, immediate dialogue with policymakers, better data on per-shipment landed costs, and collective action to propose constructive alternatives can help avoid the worst outcomes.

Bangladesh’s logistics cost was already a strategic constraint, the new tariffs raised the stakes, making reform ever more urgent.